Roper Technologies – Overview and Q3 2025 Results

It is my pleasure to provide you with an overview of the key highlights regarding Roper Technologies’ third quarter (Q3) 2025.

Before that, let me briefly introduce the company.

Roper Technologies, Inc. (ROP) is included in the Nasdaq 100, S&P 500, and Fortune 1000 indices. The company stands out for its business model focused on sustainable cash flow growth and a disciplined acquisition strategy.

Company Overview

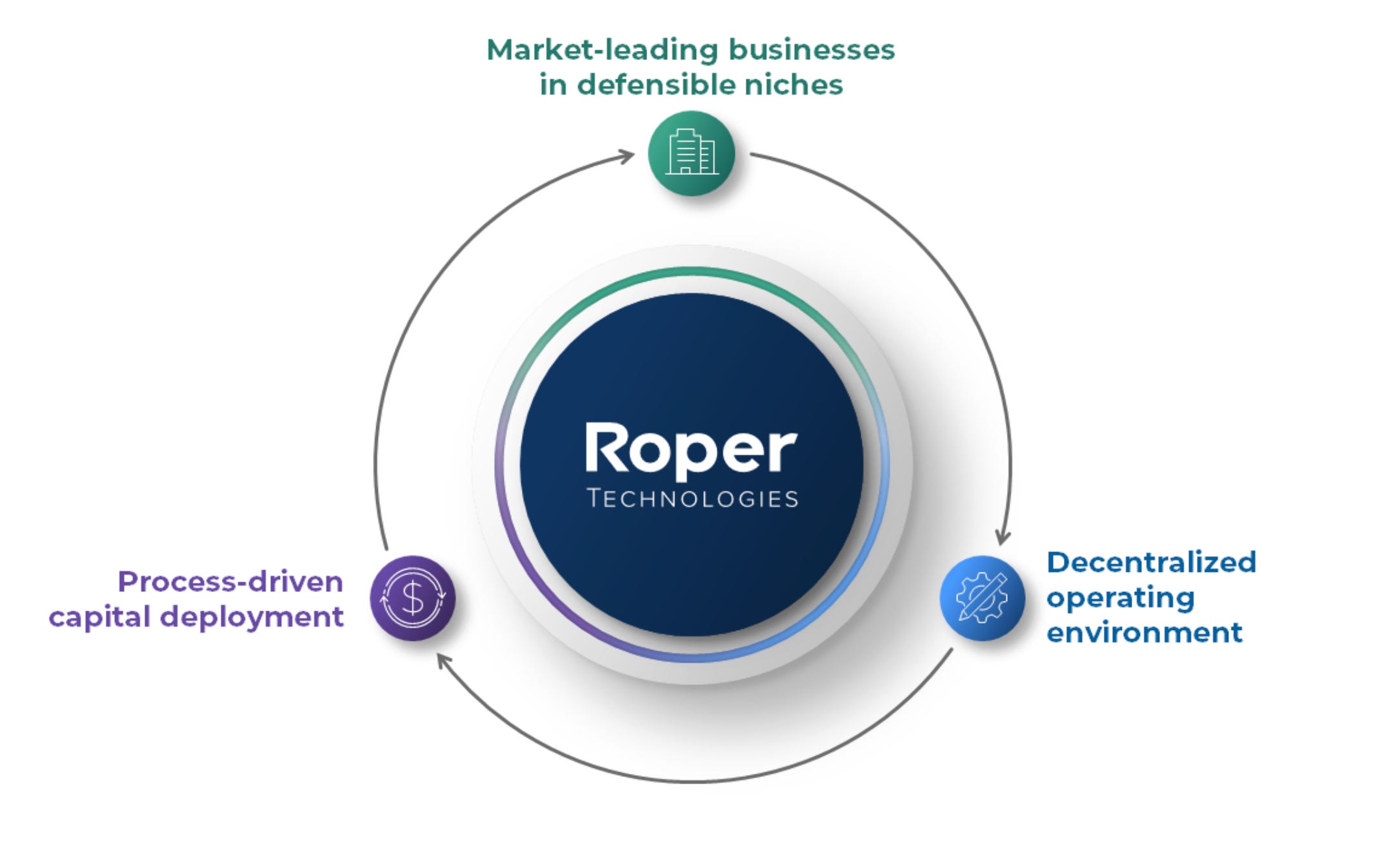

Roper Technologies manages a portfolio of market-leading businesses, each recognized for its dominant position in highly specialized industries.

Business focus: The company specializes in designing and developing vertical software and advanced technology-enabled products aimed at defensive niche markets.

Financial objective: Roper targets sustained compounding growth in its cash flows over the long term, aiming to double its free cash flow roughly every five years. Over the past three years, the trailing twelve-month (TTM) free cash flow has grown at a 17% CAGR.

Operating model: The group adopts a decentralized structure, granting each subsidiary strong autonomy to promote customer proximity and operational efficiency.

Roper Technologies: A “Serial Acquirer”?

Absolutely. Acquisitions lie at the heart of Roper’s growth strategy, often described as a “dual threat offense,” combining operational excellence with disciplined capital allocation.

Capital deployment strategy: Roper follows a rigorous, analytical, and process-driven approach to redeploy excess capital into high-quality acquisitions with strong value-creation potential.

Bolt-on acquisitions: The company continuously seeks to identify and integrate new market leaders or complementary businesses that enhance existing platforms.

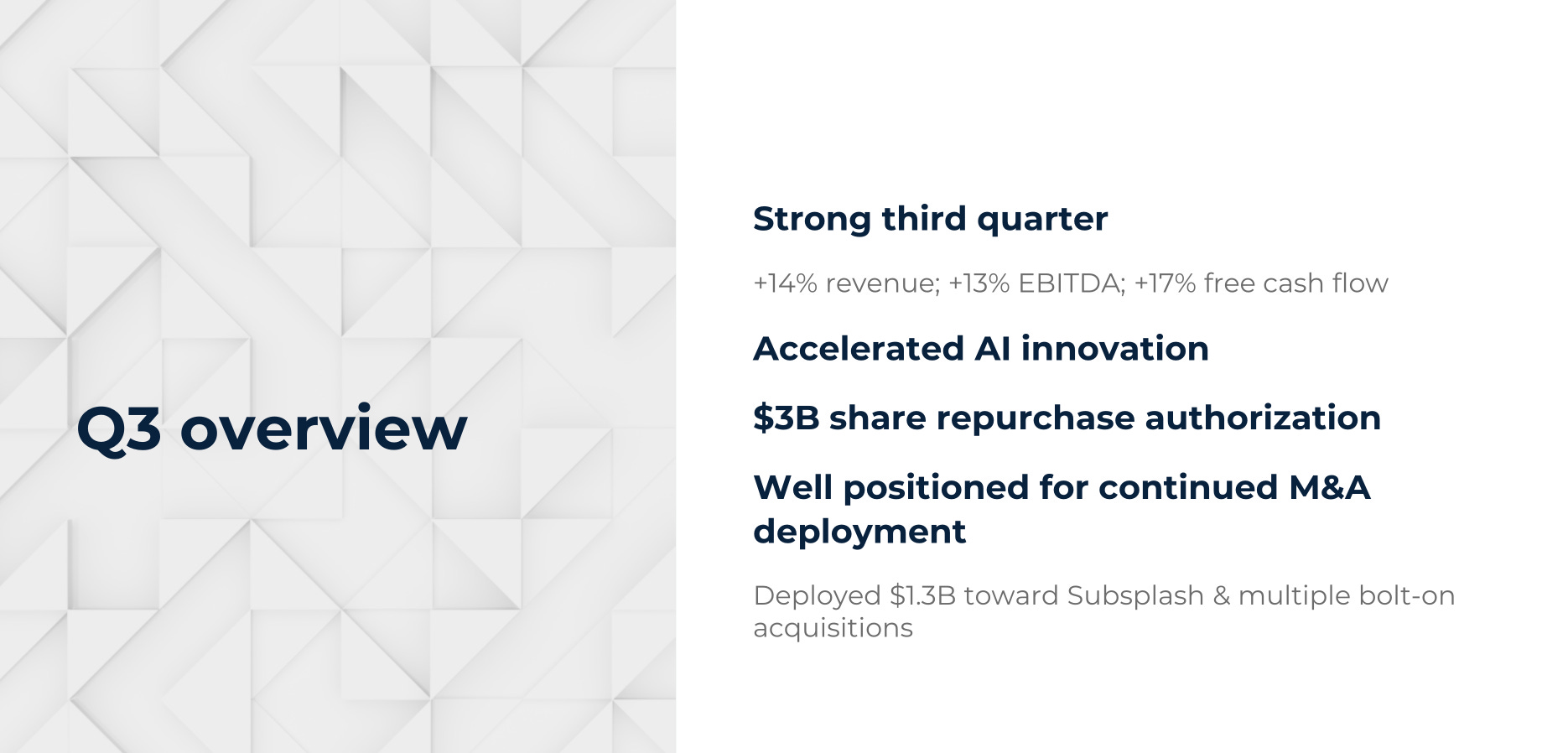

Recent activity: In Q3 2025, Roper invested $1.3 billion to acquire Subsplash and several complementary businesses.

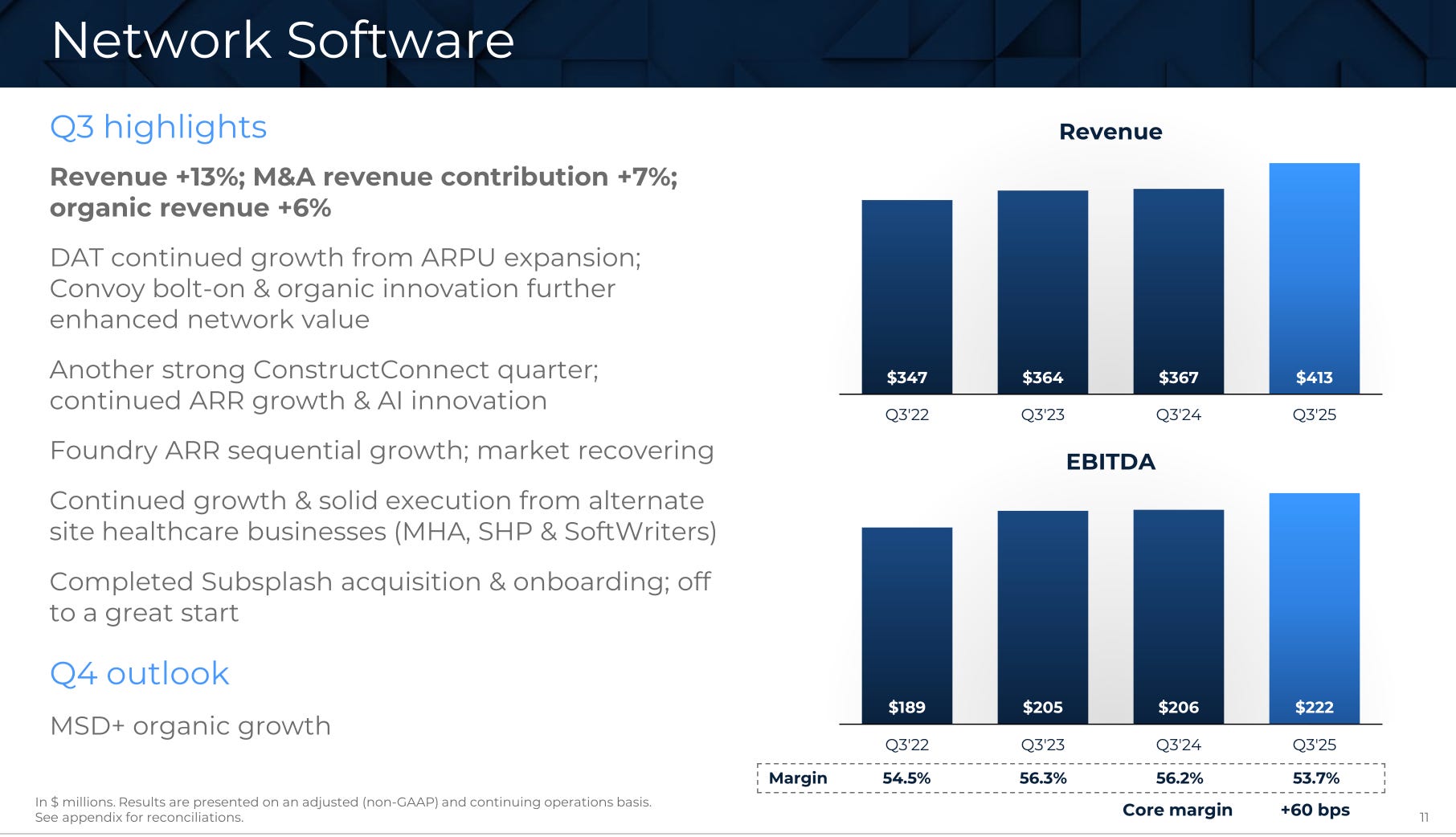

Convoy was integrated into DAT,

Orchard Software joined Clinisys.

These deals strengthen Roper’s ecosystem, particularly in areas related to artificial intelligence.

Capacity and outlook: Roper maintains an annual deployment capacity exceeding $5 billion and a robust acquisition pipeline. Despite launching a $3 billion share repurchase program, mergers and acquisitions remain the top priority for long-term growth.

Q3 2025 Summary: Performance and Outlook

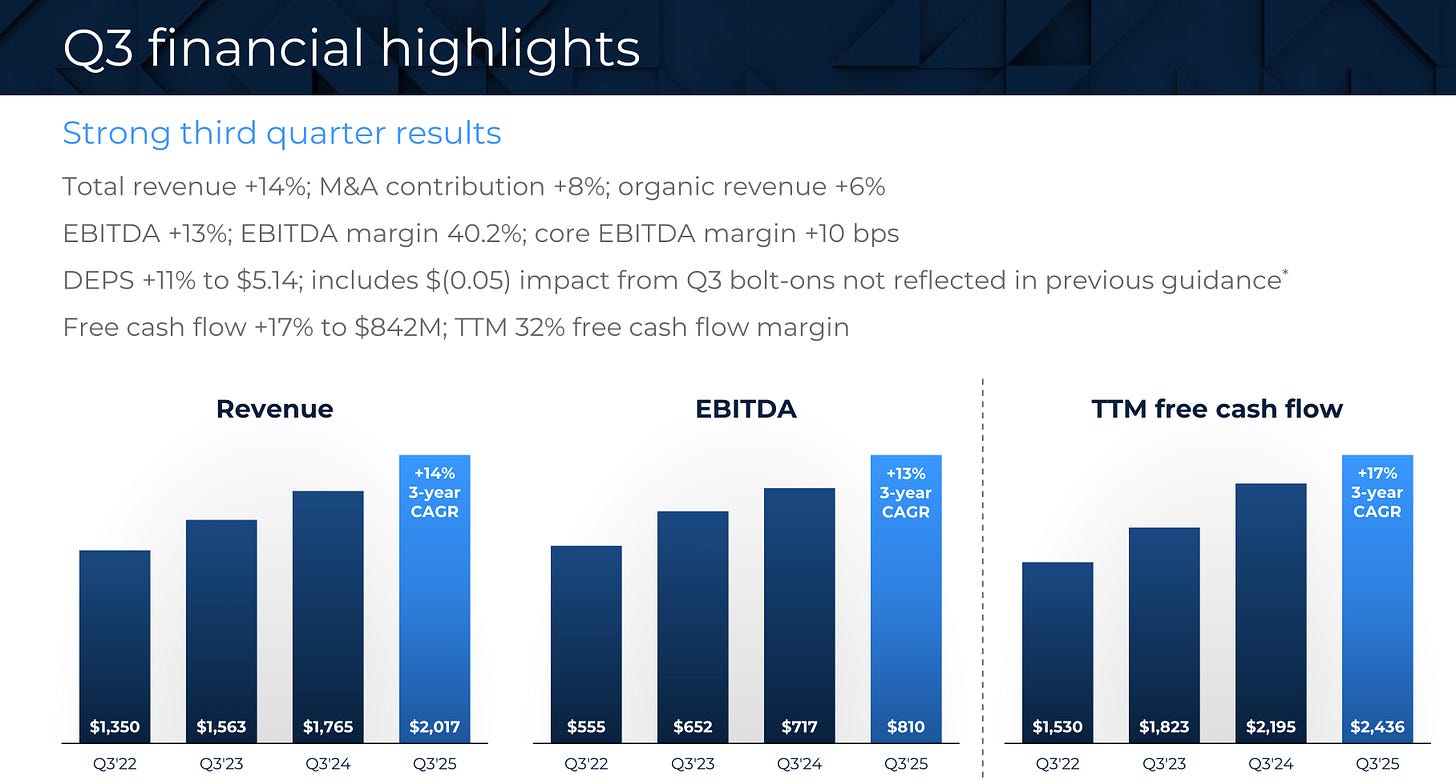

Roper Technologies delivered a solid third quarter, highlighting the resilience and quality of its business model.

1. Financial Performance and Cash Flow Generation

Revenue: Up 14% to $2.02 billion, including 6% organic growth.

Adjusted EBITDA: Up 13% to $810 million.

Adjusted DEPS: Up 11% to $5.14.

Free Cash Flow: Up 17% to $842 million.

TTM FCF margin: 32%, totaling $2.436 billion, with a 17% 3-year CAGR.

2. Financial Structure and Capital Allocation

Investment capacity: Over $5 billion annually, supported by a strong balance sheet.

Acquisitions: $1.3 billion spent on Subsplash and bolt-ons.

Share buyback: $3 billion authorized, to be executed opportunistically.

Leverage: Net debt-to-EBITDA ratio at 3.0x.

3. Innovation and Artificial Intelligence Potential

Roper is emerging as a major player in AI-driven vertical software.

TAM expansion: AI integration broadens the addressable market and creates new value for customers through automation and digitization.

Competitive edge: Subsidiaries benefit from deeply integrated software systems built on decades of proprietary data and expertise.

Concrete use cases:

Aderant and CentralReach: ~75% of new bookings are AI-enabled products.

Deltek: 40+ AI-based features.

DAT: Advanced freight-matching capabilities through AIML.

Timeline: Significant financial impact expected from 2027 onward.

4. 2025 Outlook

Revenue growth: ≈13% (unchanged).

Organic growth: Revised to ≈6% (from 6–7%).

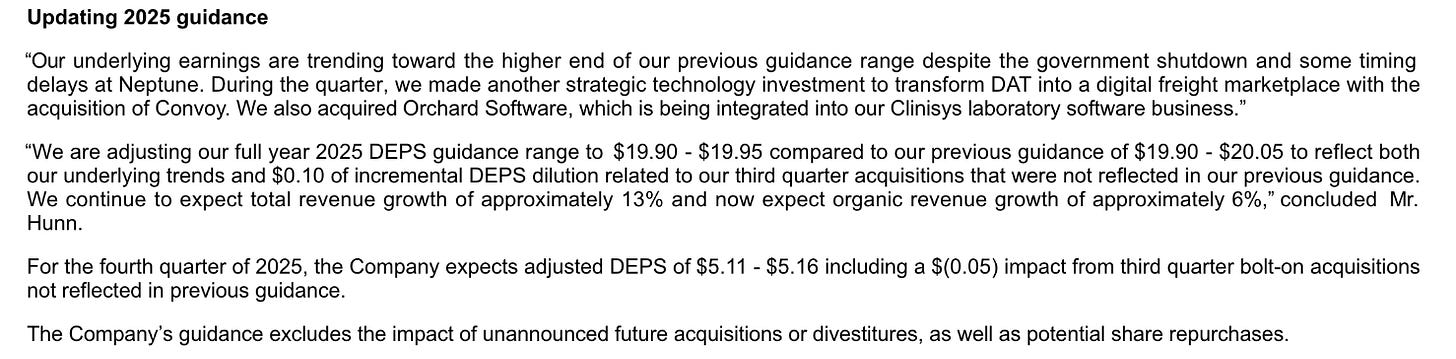

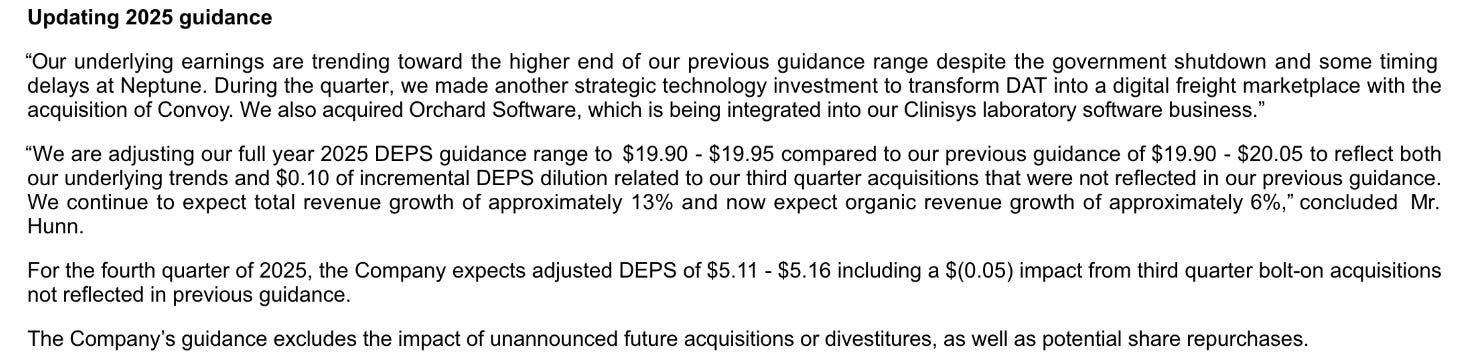

Adjusted DEPS: Now expected between $19.90–$19.95, reflecting $0.10 dilution from acquisitions.

Q4 2025 DEPS: Expected between $5.11–$5.16.

Risks and Areas of Concern

Despite its strong fundamentals, Roper faces several short- and medium-term challenges.

1. Macroeconomic headwinds impacting organic growth:

Deltek (GovCon): Slower government-related activity due to political uncertainty and potential budget shutdowns.

Neptune (TEP): Delivery delays linked to new copper tariffs; orders postponed, not lost.

2. Segment outlook for Q4:

Application software: Mid-single-digit organic growth expected, weighed by public sector caution.

Technology-enabled products: Low-single-digit growth expected due to tough comps and deferred orders.

3. Acquisition-related risks:

Convoy (DAT): Not yet profitable but strategically critical for AI-driven freight automation.

Broader risks include higher interest rates, inflationary pressures, cybersecurity threats, geopolitical instability, labor shortages, and potential intangible asset impairments.

Conclusion

Roper Technologies achieved an excellent Q3 2025, with 14% revenue growth and a 17% increase in free cash flow.

The company continues to execute its disciplined capital deployment strategy, investing $1.3 billion in acquisitions and launching a $3 billion buyback program.

With its focus on AI-driven innovation, Roper is well-positioned for long-term growth. However, organic growth guidance has been trimmed to about 6% due to temporary headwinds at Deltek and Neptune.

The group retains more than $5 billion in M&A capacity and maintains a solid balance sheet (Net debt/EBITDA = 3.0x), underscoring its financial strength and strategic flexibility.

My Opinion

Roper is clearly a high-quality company with excellent fundamentals. However, its leverage ratio of 3x EBITDA warrants close monitoring. Revenue, cash flow, and earnings per share continue to demonstrate robust performance.

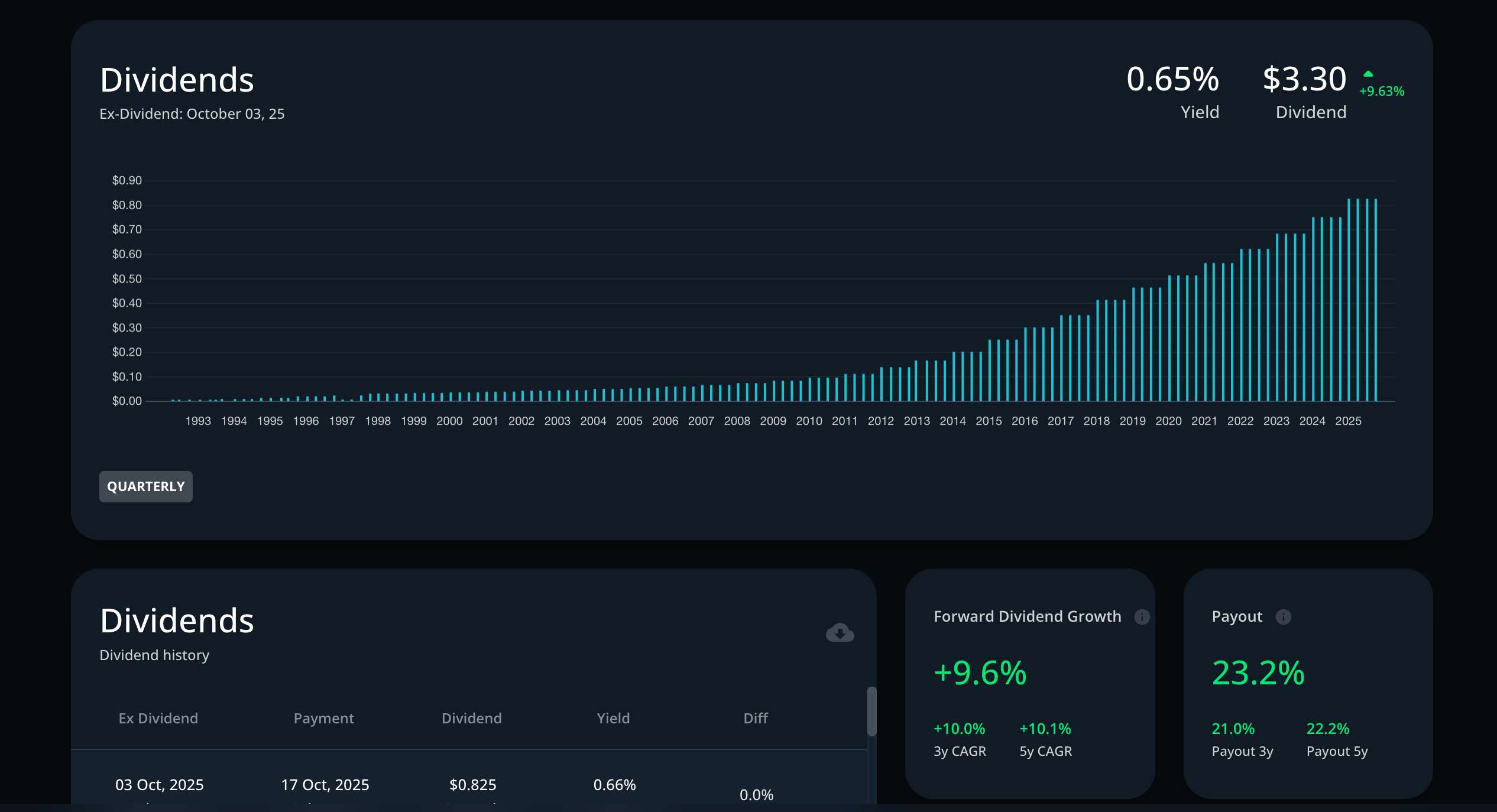

The dividend, growing over 10% per year, signals confidence and balance-sheet strength.

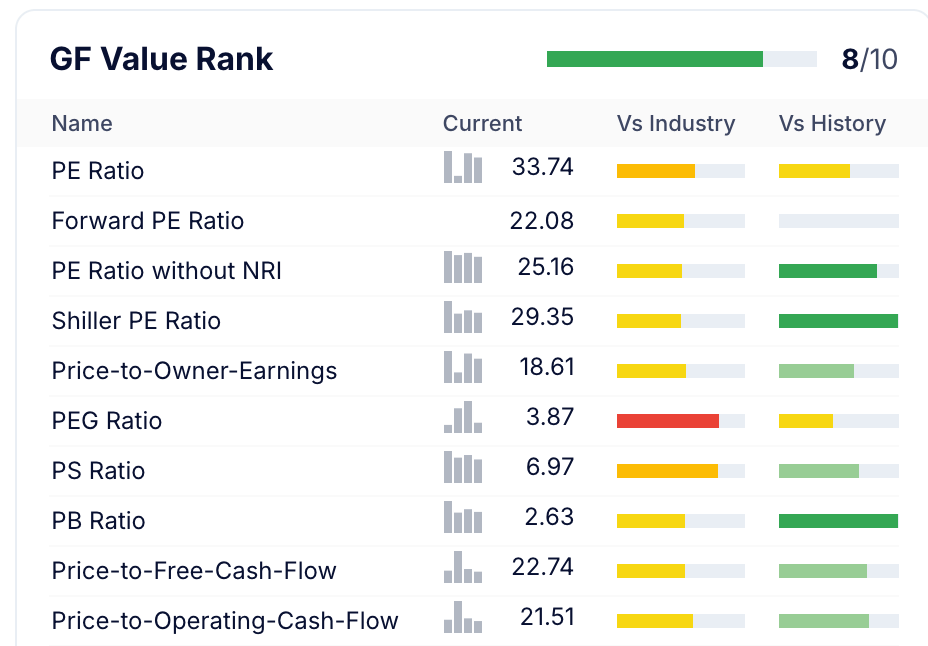

From a valuation standpoint, while the P/E ratio above 30x appears expensive, the P/FCF ratio of about 22x looks more appealing — below its historical median, with a potential support zone around 19x.

After a 20% correction over recent years, the stock may still face short-term downside risk but is approaching an attractive entry point for medium- to long-term investors.

Technically, the price recently touched its 75-period moving average, a rare occurrence, while the RSI around 40 suggests limited downside momentum.

At this stage, opening a position could prove interesting, although I personally prefer to wait for an even more attractive entry point before allocating capital elsewhere.

Finally, while Roper’s gross and net margins remain impressive, its return on invested capital (ROIC) is still below 10%, an aspect worth considering in a full assessment of the company.